In Pakistan, small-scale retailers predominantly operate within a cash-based economy, limiting their economic mobility and business growth. Given that traditional financial systems are largely centered on Western practices developed in the Global North, swaths of users from different cultural and educational backgrounds are denied participation. This holds especially true in Pakistan where Islamic law prohibits the charging or paying of interest – a fundamental model in traditional banking.

In 2019, only 2.4% of the population had access to credit through a formal financial institution. Without credit access, merchants face unpredictable cash-flow cycles, leaving them cash-strapped when restocking, leveraging bulk purchase discounts, or managing unexpected operational expenses. Furthermore, it leaves them vulnerable to informal predatory lending practices.

In 2020, we partnered with Standard Chartered, Unilever Pakistan, IDEO’s Last Mile Money Initiative and Finja, a Pakistani digital financial services provider, to increase access, adoption, and usage of Finja’s digital credit service amongst small-scale, fast-moving consumer goods (FMCG) retailers. Our collective goal was to redesign Finja’s digital credit app into a reliable tool that would allow merchants to buy stock on credit, expand their businesses, and achieve economic mobility.

According to a 2021 Macro Pakistani study, Pakistan has around 2 million retailers. A separate study conducted by Finja, found that 72% of all retailers engage in informal credit practices. With a retail sector conservatively estimated at $152 billion, a shift towards a credit-based economy has the profound potential to empower merchants like corner store sellers and market stall vendors to foster business growth and transform their livelihoods.

Building Trust: Finja’s Journey with Islamic Compliance and Accessibility

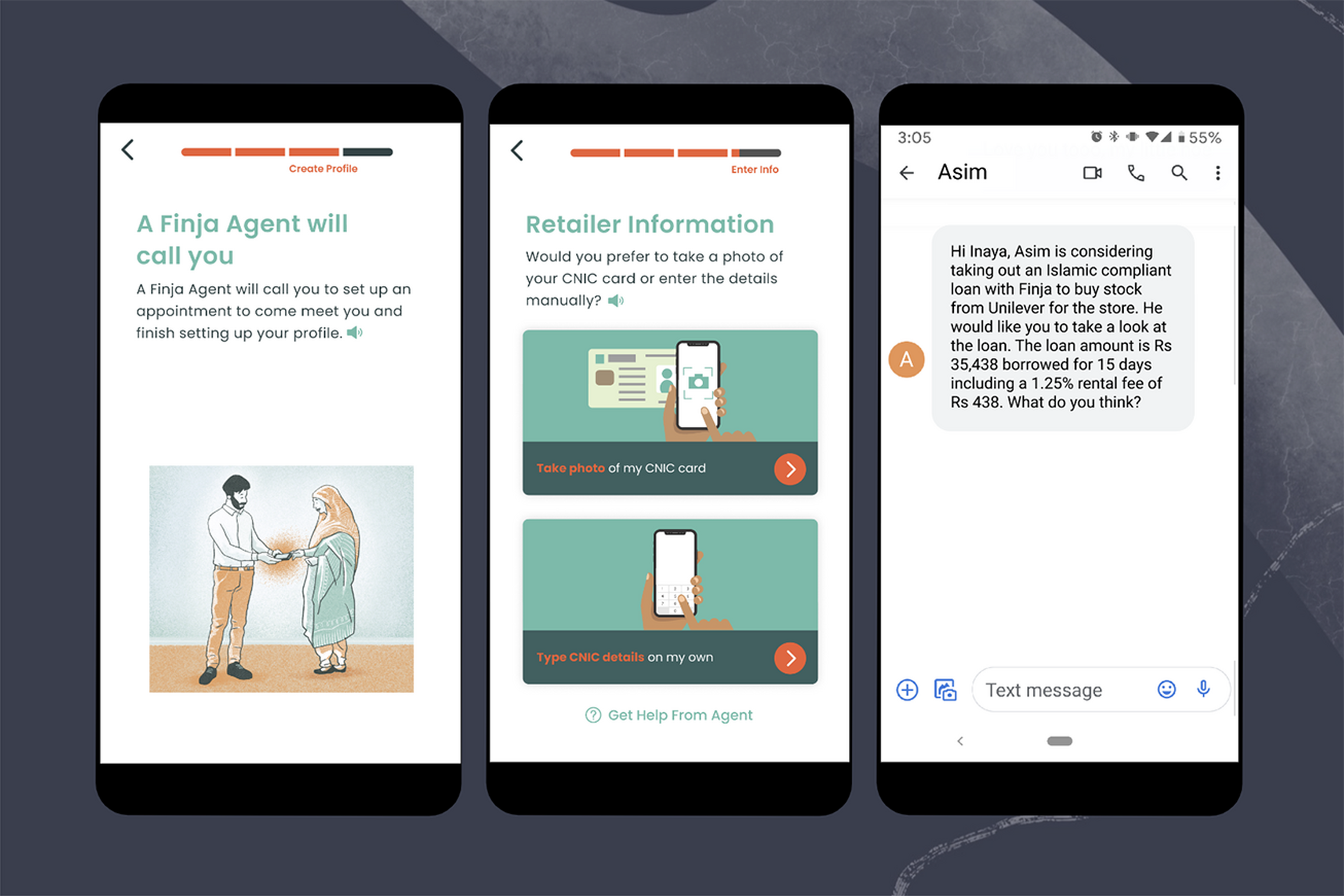

We collaborated with Ideate Innovation, a local human-centered design firm, to identify the challenges impacting a retailer’s likelihood to leverage a digital financial product. After conducting interviews with retailers of varying sizes and financial literacy levels in Islamabad and Lahore, we determined that Islamic compliance was paramount to the app’s success.

The vast majority of retailers were hesitant to utilize credit unless it was approved by a mufti – a Muslim legal expert. Without clear and consistent communication of Islamic compliance, the app would not achieve widespread adoption. The second greatest obstacle was Finja’s accessibility amongst a primary user group with limited digital confidence. Many merchants still maintain their accounting using paper records, a process often managed by multiple family members and transitioning to a fully digital service felt like a high-risk leap for many.

Following our research phase, we tested multiple prototypes gaining deeper insights into the needs of micro-merchants in Pakistan which ultimately led to six key principles:

Communicate Islamic compliance clearly and consistently.

Provide a combination of tech and touch support during onboarding to build digital confidence.

Validate and protect app from misuse to foster trust.

Accommodate the busy lives and schedules of retailers

Incentivize use as cash remains king in Pakistan’s slowly evolving digital finance ecosystem

Incorporate multiple users as families are key stakeholders in financial decisions

We identified a number of design opportunities within the app’s UX and onboarding process to adhere to these principles. For instance, to enhance users’ trust in the app’s Islamic compliance, we integrated pop-up screens featuring written, audio and video messages and share buttons enabling users to spread awareness amongst their communities. To boost digital confidence, we leveraged text-to-speech functionality, making the app accessible to users regardless of literacy levels. To reduce user effort, we simplified inputs required in high-stakes moments and explored optical character recognition (OCR) to auto populate information from users’ national identity cards.

Reintroducing: Finja

In less than a year after re-launching the app, 20.9k retailers were onboarded and over $11.2k in loans were disbursed. Those who leveraged Finja’s credit services saw a 58% higher average in sales and a 32% increase in the number of products. By prioritizing these six principles in Finja’s UX redesign and the guided onboarding process, merchants felt confident that the app was aligned with their religious values, and navigated its interface with relative ease when taking out and repaying loans. The majority of merchants interviewed, 67%, expressed their inability to find a good alternative to Finja for accessing credit.

As part of the relaunch, Finja collaborated with Unilever’s Guddi Baji initiative to demonstrate how credit access could be a powerful tool beyond economic mobility for women entrepreneurs in rural Pakistan. Among the app’s early adopters were 47 Guddi Bajis, who served as community influencers for Unilever products. Through digital credit, the Guddi Baji’s no longer depended on male family members to borrow money, which opened space for their financial independence. Additionally, for these remote retailers, Finja’s app eliminated the need to travel long distances to secure and repay loans which freed them from choosing between work, childcare, and access to credit.

Crossing the Chasm

In recent years, Pakistan has experienced a notable surge in fintech startups, driven in part by government funding and investments. Despite this growth, digital financial services continue to operate on the fringes of society, accessible to a privileged minority, due to obstacles stemming from an exclusionary financial system. As momentum to expand the fintech sector continues, human-centered design can play a critical role in addressing the gaps created by the traditional financial system and creating services that are relevant to the majority. By crossing the chasm into mainstream use, apps like Finja have the potential to support over 180 million small scale retailers in underbanked communities around the world to improve their economic livelihoods.